I only really understood compound interest after I stopped reading descriptions of it and calculated a few examples by hand. The formula looks more awkward than the idea behind it. You start with an amount, add interest, then the next round of interest is calculated on the new, slightly larger balance.

This article is for the manual calculation: how to work through the formula yourself, how to handle monthly compounding, and how to sanity-check the answer before using a calculator. If you just want the answer quickly, use the Compound Interest Calculator. If you are building a wider savings or investment plan, compare the result with the Savings Calculator or Investment Calculator.

What Compound Interest Means in Plain Terms

Compound interest means interest is added to the balance, and future interest is calculated on that updated balance. Simple interest keeps calculating from the original amount only. Compound interest keeps updating the base number.

That distinction matters because the gap is small at first and much larger later. A one-year example may barely look different. A ten-year or thirty-year example can look completely different, especially when money is left alone to grow.

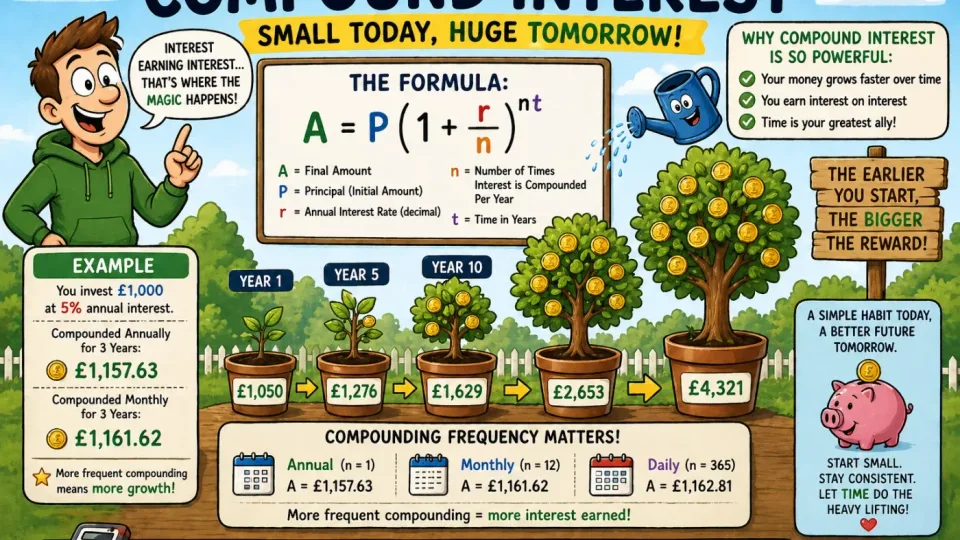

The Compound Interest Formula

The standard formula is:

A = P (1 + r/n)nt

Where:

- A = final amount

- P = starting principal

- r = annual interest rate as a decimal

- n = number of compounding periods per year

- t = time in years

The most common mistake is using the percentage directly. Five percent is not 5 in the formula. It is 0.05. Seven percent is 0.07. Twelve percent is 0.12.

How to Calculate Compound Interest Step by Step

Use this process when you want to calculate compound interest manually:

- Write down the starting amount.

- Convert the annual interest rate into a decimal.

- Decide how often interest compounds.

- Divide the annual rate by the compounding frequency.

- Multiply the number of years by the compounding frequency.

- Put those values into the formula.

- Subtract the starting amount from the final amount to find the interest earned.

Example 1: Basic Annual Compounding

Suppose you put £1,000 into an account earning 5% per year for 3 years, compounded annually.

Because the interest compounds once per year, n = 1.

A = 1000 × (1 + 0.05/1)1×3

A = 1000 × 1.053

A = 1000 × 1.157625 = £1,157.63

The final balance is £1,157.63. The interest earned is £157.63.

Example 2: Monthly Compounding

Now use the same starting amount, rate, and time period, but compound monthly instead of annually.

Starting amount: £1,000

Annual rate: 5% or 0.05

Compounding frequency: 12

Time: 3 years

A = 1000 × (1 + 0.05/12)12×3

A = 1000 × (1.0041667)36

A ≈ £1,161.47

Monthly compounding produces a slightly higher result than annual compounding because interest is added to the balance twelve times per year instead of once.

Annual vs Monthly Compounding Comparison

For the same £1,000 at 5% over 3 years:

- Annual compounding gives about £1,157.63.

- Monthly compounding gives about £1,161.47.

- The difference is about £3.84.

That difference is modest over three years on a small balance. It becomes more noticeable with larger balances, higher rates, or longer time periods. The Interest Calculator is useful when you want to compare simple and compound interest side by side.

Example 3: Regular Monthly Deposits

The basic compound interest formula is cleanest when there is one starting amount and no extra deposits. Real saving is often messier. You might start with nothing and add money every month, or start with a lump sum and keep contributing.

Imagine you save £150 per month for 5 years and earn 4% annually, compounded monthly. You contribute £9,000 in total before interest.

A contribution-based calculation treats each monthly deposit as having its own time to grow. The first £150 compounds for almost the full five years. The final £150 barely compounds at all. That is why regular-deposit examples are better handled with the Investment Calculator or Savings Calculator rather than the single-lump-sum formula.

As a rough illustration, £150 per month for 5 years at 4% compounded monthly grows to about £9,950. The deposits provide £9,000, and compounding adds roughly £950.

Example 4: Savings Growth

For cash savings, the key question is usually less dramatic: how much will this account add over time?

Suppose you have £5,000 in savings at 4.5% for 2 years, compounded monthly.

A = 5000 × (1 + 0.045/12)24

A ≈ £5,470.05

The interest earned is about £470.05. For savings accounts, also check whether the advertised rate is AER, whether tax applies to the interest, and whether bonuses expire. The article on comparing savings account interest is a better fit for account-shopping decisions.

Example 5: Investment Growth

Investment examples need more caution because returns are not fixed like a savings rate. Still, compound growth is useful for modelling scenarios.

If £10,000 grows at an average 7% per year for 20 years, compounded annually:

A = 10000 × 1.0720

A ≈ £38,696.84

The interesting part is not just the final number. It is the shape of the growth. The first few years feel slow. Later years do more of the visible work because returns are being earned on a much larger balance. Use the Investment Return Calculator when you want to compare actual starting and ending values, and the compound interest and wealth-building guide for the broader planning context.

Example 6: Debt Compounding Downside

Compound interest is not automatically good. It depends which side of the calculation you are on.

Suppose a £3,000 balance is charged at 20% annual interest, compounded monthly, and no repayments are made for one year.

A = 3000 × (1 + 0.20/12)12

A ≈ £3,658.17

That is about £658.17 of interest in one year. Real loans and credit cards include repayments, minimum-payment rules, fees, and APR terms, so the exact number can differ. The point is simpler: when unpaid interest is allowed to join the balance, the debt can become harder to clear than the headline rate suggests.

What Each Part of the Formula Changes

- Principal: A larger starting amount gives compounding more to work with.

- Rate: A higher rate changes the result sharply over long periods.

- Frequency: Monthly compounding usually beats annual compounding, but the difference is often smaller than people expect.

- Time: Time is the part people underestimate most.

If you only need a quick doubling estimate, use the Rule of 72 Calculator. The rule is simple: divide 72 by the annual rate to estimate how many years it takes money to double. At 6%, money roughly doubles in 12 years.

Simple vs Compound Interest

Simple interest is calculated only on the original principal. Compound interest is calculated on the principal plus previous interest.

With £1,000 at 5% for 10 years:

- Simple interest earns £500, ending at £1,500.

- Annual compound interest ends at about £1,628.89.

- The extra £128.89 is interest earned on earlier interest.

That gap is why the phrase “interest on interest” is useful, even if it sounds a bit too neat. It is also why compounding is more visible over decades than over months.

Common Manual Calculation Mistakes

Using 5 instead of 0.05

Percentages need converting before they go into the formula. Five percent becomes 0.05.

Mixing annual and monthly numbers

If interest compounds monthly, divide the annual rate by 12 and multiply the years by 12. Do not use the annual rate with monthly periods.

Using the lump-sum formula for monthly deposits

The standard formula handles one starting amount. Regular deposits need a future-value-of-annuity calculation or a calculator built for contributions.

Assuming investment returns arrive smoothly

A 7% average return does not mean 7% every year. Real investments move unevenly, so treat projections as scenarios rather than promises.

Frequently Asked Questions

What is the compound interest formula?

The formula is A = P(1 + r/n)nt. A is the final amount, P is the starting principal, r is the annual rate as a decimal, n is the number of compounding periods per year, and t is the number of years.

How do I calculate monthly compound interest?

Convert the annual rate to a decimal, divide it by 12, multiply the number of years by 12, then use those values in the compound interest formula.

Can I use the same formula for monthly deposits?

Not cleanly. The basic formula is for a single starting amount. Monthly deposits need a contribution-based future value calculation because each deposit has a different amount of time to grow.

Why does monthly compounding give a higher result than annual compounding?

Monthly compounding adds interest to the balance sooner, so later months earn interest on earlier months' interest. The difference is usually small over short periods but grows with time, rate, and balance size.

Is compound interest good for debt?

No. Compounding works against you when you owe money because unpaid interest can become part of the balance that future interest is charged on.

Conclusion

To calculate compound interest yourself, keep the process boring and exact: convert the rate, match the compounding frequency to the time period, apply the formula, then subtract the starting amount to see the interest earned.

Manual calculation is useful because it shows what the calculator is doing. Once you understand the moving parts, use the Compound Interest Calculator for quick lump-sum examples, the Investment Calculator for regular contributions, and the Savings Calculator for savings goals.