My first experience of VAT as a business owner was realising I had been calculating it incorrectly — adding it on top rather than working out what was already included.

VAT (Value Added Tax) is a percentage added to the price of most goods and services. Whether you're running a business, checking receipts, or working out prices, knowing how to calculate VAT is essential.

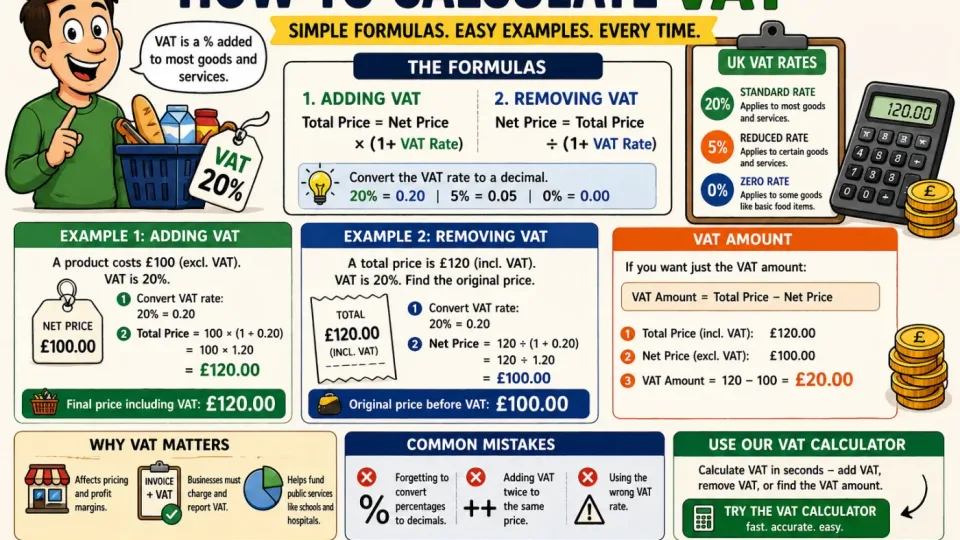

This guide explains how to calculate VAT step by step, including how to add VAT, remove VAT, and work with different VAT rates.

---What Is VAT?

VAT is a consumption tax applied to goods and services. In the UK, the standard VAT rate is typically 20%, although reduced rates such as 5% and 0% may apply to certain items.

When VAT is applied, it increases the total price paid by the customer.

---VAT Formula

There are two main VAT calculations:

1. Adding VAT:

Total Price = Net Price × (1 + VAT Rate)

2. Removing VAT:

Net Price = Total Price ÷ (1 + VAT Rate)

Always convert the VAT rate into a decimal. For example:

- 20% = 0.20

- 5% = 0.05

How to Add VAT

Example 1: Adding VAT to a Price

You have a product that costs £100 (excluding VAT). VAT is 20%.

Step 1: Convert VAT rate.

20% = 0.20

Step 2: Apply formula.

Total Price = 100 × (1 + 0.20)

Total Price = 100 × 1.20 = £120

The final price including VAT is £120.

---How to Remove VAT

Example 2: Removing VAT from a Price

You have a total price of £120 including VAT at 20%. You want to find the original price.

Step 1: Convert VAT rate.

20% = 0.20

Step 2: Apply formula.

Net Price = 120 ÷ 1.20 = £100

The original price before VAT is £100.

---How to Calculate the VAT Amount

If you want just the VAT amount:

VAT Amount = Total Price − Net Price

Using the example above:

VAT = £120 − £100 = £20

---Different VAT Rates

In the UK, common VAT rates include:

- 20% – Standard rate

- 5% – Reduced rate (e.g. some energy bills)

- 0% – Zero-rated goods (e.g. basic food items)

Always check which rate applies before calculating VAT.

---Why VAT Matters

VAT affects pricing, profit margins, and business cash flow. Businesses need to:

- Charge VAT on sales (if registered)

- Reclaim VAT on purchases

- Calculate VAT correctly for invoices

Incorrect VAT calculations can lead to pricing errors or tax issues.

---Use the VAT Calculator

To calculate VAT instantly, use our VAT Calculator.

You can also use the Percentage Calculator to work with VAT percentages, or the Discount Calculator when calculating final sale prices.

---Common VAT Mistakes

Forgetting to Convert Percentages

Always convert VAT rates into decimals before using formulas.

Adding VAT Twice

Check whether VAT is already included in the price before adding it again.

Using the Wrong Rate

Different goods and services have different VAT rates.

---Frequently Asked Questions

What is VAT?

VAT is a tax added to most goods and services.

How do I calculate VAT?

Multiply the net price by (1 + VAT rate).

How do I remove VAT from a price?

Divide the total price by (1 + VAT rate).

What is the UK VAT rate?

The standard rate is usually 20%.

---Conclusion

VAT is straightforward once you understand the formulas. You either multiply to add VAT or divide to remove it.

For quick calculations, use the VAT Calculator.

The Two Calculations People Confuse

There are two distinct VAT calculations, and confusing them is the source of most errors. Adding VAT to a net price: multiply the net amount by 1.20 (for 20% VAT) to get the gross price. So a £100 net price becomes £120 gross. Extracting VAT from a gross price: divide the gross amount by 1.20 to get the net, then subtract to find the VAT element. So a £120 gross price contains £100 net and £20 VAT. The mistake people make is calculating 20% of the gross price: 20% of £120 is £24, not £20. The VAT element in a VAT-inclusive price is always calculated by dividing, not by taking a percentage of the gross figure. This matters for invoicing, VAT returns, and any situation where you need to separate VAT from a total you've been charged.

VAT Rates and When They Apply

The UK operates three VAT rates, and applying the wrong one is a compliance risk. The standard rate of 20% applies to most goods and services. The reduced rate of 5% applies to specific categories including domestic fuel and power, children's car seats, and some energy-saving materials. Zero-rated items (0% VAT) include most food, children's clothing, books, and newspapers — importantly, zero-rated items are still VAT taxable supplies, they just have a 0% rate, which means VAT-registered businesses can reclaim VAT on costs related to zero-rated sales. Exempt supplies (such as financial services, insurance, and most residential lettings) are different from zero-rated: businesses making only exempt supplies cannot register for VAT and cannot reclaim input VAT. Understanding which category your sales fall into determines both your VAT obligations and your right to reclaim input tax.

VAT Registration and the Threshold

VAT registration becomes compulsory when your taxable turnover exceeds the registration threshold in any rolling 12-month period — currently £90,000 as of 2024. Turnover here means the value of your VAT taxable supplies (standard-rated, reduced-rate, and zero-rated sales), not profit. You must register within 30 days of the end of the month in which you exceeded the threshold, and charge VAT from the date you were required to register. Voluntary registration is possible below the threshold and can be advantageous if your customers are mainly businesses who can reclaim the VAT, or if you have significant VAT-able costs you want to recover. The decision involves weighing the administrative burden of quarterly VAT returns against the cash flow and reclaim benefits.

Practical VAT Accounting

For everyday business use, the key habit is keeping output VAT (VAT you charge on sales) and input VAT (VAT you pay on purchases) clearly separated. Output VAT is a liability — money collected on behalf of HMRC that you must pay over on your VAT return. Input VAT is an asset — money you can reclaim. The difference is what you either pay to or reclaim from HMRC each quarter. Most businesses submit quarterly VAT returns online via Making Tax Digital-compatible software. Cash accounting and flat rate schemes are available for smaller businesses and can simplify the administration, but each has conditions and trade-offs worth understanding before choosing. Getting the basic arithmetic right — and keeping records that clearly show the net, VAT, and gross elements of each transaction — is the foundation of staying compliant.