A business I reviewed a few years ago had £180,000 in annual revenue and the owner was convinced he was making good money. His calculation was simple: revenue minus rent, staff, and stock costs. What he had not counted was everything else — and "everything else" turned out to be nearly £40,000 per year in costs he either did not track or had mentally filed as too small to matter. Merchant processing fees across three payment platforms. Packaging costs that had drifted up with inflation while pricing had not been adjusted. A delivery van that was costing £600 per month in fuel, insurance, and maintenance that he was not allocating to delivery jobs. Two software subscriptions that had been on auto-renewal for two years unused. When we mapped every cost, the margin was 8% — not the 25% he believed he was running.

Why Small Costs Get Ignored

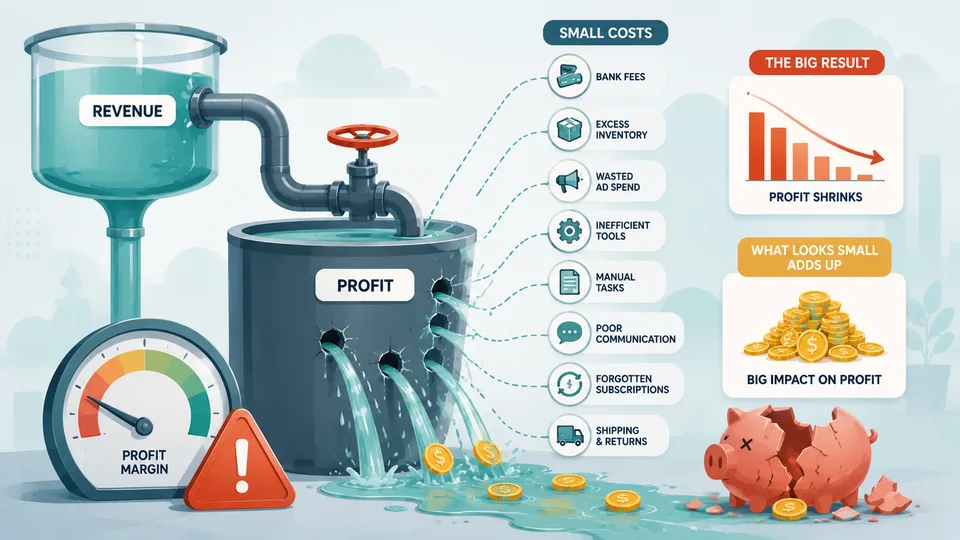

The psychology is straightforward. A £15 monthly software subscription does not feel significant. A £30 tool purchase does not seem worth tracking. A 1.9% payment processing fee disappears into the transaction and never appears as a separate line in any report. But costs have an accumulation problem: many small numbers add up to a large number, and in a business where margin is thin, that accumulation is the difference between profitability and loss. The problem is compounded by the fact that small costs tend to increase gradually over time — through price rises, through scope additions, through new tools adopted to solve specific problems that then become permanent — while being reviewed infrequently or not at all.

Margin Leakage: Where Profit Disappears Between Revenue and the Bank

Margin leakage is the gap between the gross margin implied by pricing and the net margin that actually reaches the bottom line. Common sources include: payment processing fees (1.4–2.9% of revenue), refunds and returns (varies widely, but 5–20% in e-commerce), wastage and spoilage in product businesses, discounts given informally to retain customers, and delivery costs that are not fully recharged. Each of these individually is explicable and manageable. Together they can reduce a 35% gross margin to a 20% net margin without any single obvious cause. Tracking them separately — as named line items in the management accounts rather than lumped into miscellaneous overheads — makes the pattern visible. Invisible costs cannot be managed.

The Subscription Audit Every Business Should Do Quarterly

Software subscriptions are the single most common source of unnoticed cost drift in small businesses. The typical small business accumulates tools over time: each one adopted for a specific reason, each one renewed automatically because cancelling requires effort. A quarterly subscription audit is straightforward: export every recurring charge from business bank accounts and credit cards for the last three months, list every subscription with its monthly cost, and categorise each as actively used, occasionally used, or unused. Unused subscriptions should be cancelled immediately. Occasionally used tools should be reviewed against whether the frequency of use justifies the cost or whether a free tier would suffice. Annual subscriptions should be reviewed before renewal rather than auto-renewed by default.

Pricing and Cost Drift: What Happens When You Do Not Raise Prices

Variable costs — materials, energy, postage, packaging, third-party services — tend to increase over time with inflation. If prices are not reviewed and adjusted with at least the same frequency, margin shrinks slowly and silently. A product priced at £45 with variable costs of £18 in 2022 has a contribution margin of £27. If variable costs rise to £24 by 2024 due to material and energy price increases, the contribution margin has fallen to £21 — a 22% reduction — without any change in the headline price. In a business where fixed costs have also risen, this margin compression can transform a profitable product into a marginal one. Annual pricing reviews that start from current cost structures rather than last year's prices are the basic discipline that prevents this drift.

The Operating Margin Reality Check

Operating margin — operating profit divided by revenue — tells you what proportion of revenue remains after all operating costs are covered. A business with revenue of £200,000 and operating costs of £180,000 has an operating margin of 10%. If costs increase by £15,000 through the accumulation of small expenses, operating margin falls to 2.5% — a marginal business that any disruption in revenue could push into loss. Tracking operating margin monthly rather than looking at the profit figure in isolation puts cost accumulation in context. A net profit calculator that includes all cost categories — not just the obvious ones — gives a reliable read on where the business actually stands. A gross profit calculator lets you compare margin at the product or service level, identifying which lines are carrying the weight and which are dragging on profitability.

What to Do When You Find the Leaks

Once hidden costs are mapped and quantified, the response should be proportionate and prioritised. The largest costs deserve attention first: a £4,000 per year waste reduction is more valuable than eliminating a £200 annual subscription, even though the subscription is easier to cancel. Before cutting any cost, assess its contribution to revenue or operational capacity. Some costs that appear wasteful are actually load-bearing — removing them creates a bigger problem downstream. A marketing tool that seems underused may be driving leads that are not being tracked. A delivery van that costs £600 per month may be enabling £8,000 per month in revenue that could not be generated otherwise. Cost reduction should always start with understanding what each cost is actually buying, not just how much it costs.

Setting a Cost Threshold for Automatic Review

One practical discipline that prevents cost drift is setting a threshold above which any new recurring cost requires explicit approval, and a review calendar for all existing commitments. In a small business, a threshold of £50 per month — or £600 per year — is low enough to catch meaningful costs but high enough not to create administrative burden for genuinely trivial items. Every new subscription, service contract, or recurring commitment above the threshold should require a brief justification: what is this cost for, what does it produce, and how will we measure whether it is working? The same question applied to existing costs on an annual basis — "what has this cost produced in the last year?" — surfaces commitments that have drifted from useful to habitual. The goal is not to minimise costs as an end in itself but to ensure that every pound spent is attached to a clear purpose and that the cost is reviewed when the purpose has been fulfilled or is no longer relevant. Small businesses that do this consistently find that their cost base is both lower and more intentional than those that review costs only when a profit problem forces the conversation.

The business owner I described at the start of this article did eventually map every cost. The exercise took half a day and produced a list of fourteen costs she had not been actively tracking, totalling £14,400 per year. She cancelled four software subscriptions, renegotiated her merchant processing arrangement, and started allocating delivery costs to specific jobs. Her operating margin improved within three months — not because revenue had changed, but because she could finally see where it was going.

Related calculator: Use our Profit Margin Calculator to see how small cost changes affect margin, markup, and selling price.

What to do next

Use the ideas above as a starting point — then connect them to your own numbers and related guides on Calc It Anything.

- Read the small business finance and growth guide for the wider cluster.

- Compare with Hidden Costs in Small Business: The Expenses Owners Forget.

- Compare with The Hidden Costs of Building Software.

- Run the relevant calculator on this site with your own inputs before making a decision.

Related reading

- small business finance and growth guide

- Hidden Costs in Small Business: The Expenses Owners Forget

- The Hidden Costs of Building Software

- Markup vs Margin: The Difference That Trips Up Business Owners

Frequently asked questions

Why do small costs hurt profitable businesses?

Fixed overheads and low-margin revenue mean recurring £50–£200 leaks compound across dozens of line items. Margin looks fine on paper until you aggregate subscriptions, fees, and unused seats.

How often should I review business running costs?

A lightweight quarterly pass on software, payment fees, and contractor spend catches drift early. Tie the review to one metric — gross margin or monthly burn — so it stays actionable.

Is cutting costs always the right response?

No. Cut spend that does not protect revenue or retention first. Protect customer-facing delivery and anything with measurable ROI before across-the-board austerity.