My budgets used to fail consistently until I understood that the problem was not discipline but the way I was building the plan in the first place.

What Is a Budget?

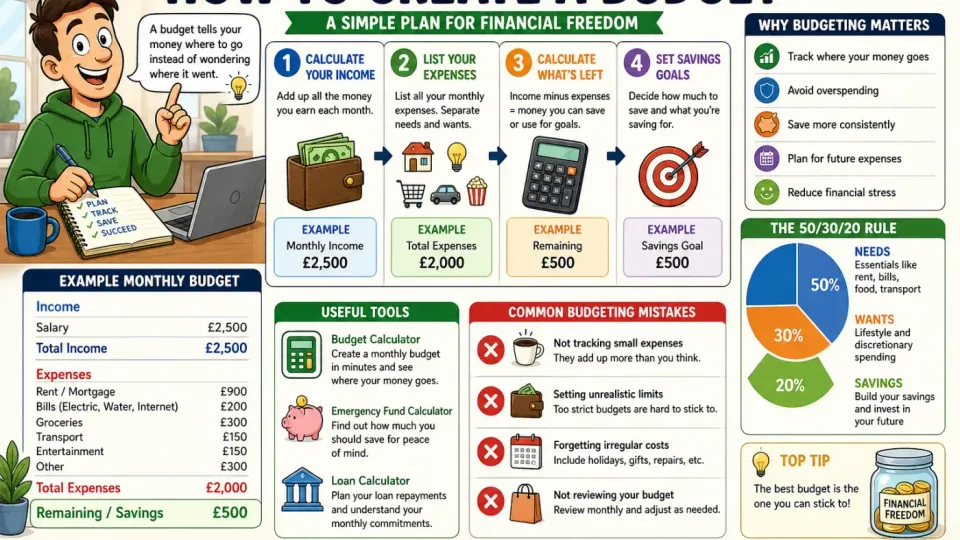

A budget is a simple plan that shows how much money you earn and how you spend it. It helps you control your finances, avoid overspending, and make sure you have enough money for important goals like saving or paying off debt.

Creating a budget is one of the most effective ways to improve your financial situation.

---Why Budgeting Matters

A budget helps you:

- Track where your money goes

- Avoid overspending

- Save more consistently

- Plan for future expenses

- Reduce financial stress

How to Create a Budget Step by Step

Step 1: Calculate Your Income

Start by working out how much money you receive each month.

This may include:

- Salary or wages

- Freelance income

- Side income

- Benefits or other payments

Example:

Monthly income = £2,500

Step 2: List Your Expenses

Next, list all your monthly expenses.

Split them into two categories:

Fixed expenses:

- Rent or mortgage

- Bills

- Subscriptions

- Loan payments

Variable expenses:

- Food

- Transport

- Entertainment

- Shopping

Example:

Total expenses = £2,000

Step 3: Calculate Your Remaining Money

Remaining = Income − Expenses

£2,500 − £2,000 = £500

This is the amount you can save, invest, or use for extra spending.

---Step 4: Set Savings Goals

Decide how much of your remaining money you want to save.

Common goals include:

- Emergency fund

- Travel

- Buying a home

- Paying off debt

The 50/30/20 Budget Rule

A simple budgeting method is the 50/30/20 rule:

- 50% needs (rent, bills, essentials)

- 30% wants (lifestyle spending)

- 20% savings

This provides a balanced approach without overcomplicating things.

---Example Budget

Monthly income: £2,500

- Needs (50%) = £1,250

- Wants (30%) = £750

- Savings (20%) = £500

Use the Budget Calculator

To create a budget quickly, use our Budget Calculator.

You can also use the Emergency Fund Calculator to plan savings, or the Loan Calculator to manage debt payments.

---Common Budgeting Mistakes

Not Tracking Small Expenses

Small purchases can add up quickly over time.

Setting Unrealistic Limits

If your budget is too strict, it’s harder to stick to.

Forgetting Irregular Costs

Include occasional expenses like holidays or repairs.

---Frequently Asked Questions

What is a budget?

A budget is a plan for managing your income and expenses.

How do I start budgeting?

Track your income, list your expenses, and set spending limits.

What is the best budgeting method?

The 50/30/20 rule is a simple and effective starting point.

Why is budgeting important?

It helps you control spending and achieve financial goals.

---Conclusion

Creating a budget is one of the simplest ways to take control of your finances. By tracking your income and expenses, you can make better decisions and build long-term financial stability.

For an easy way to get started, use the Budget Calculator.

Why Budgets Fail and How to Make One That Doesn't

Most budget failures trace back to one of three problems: starting from aspirational numbers rather than actual spending, building a budget that doesn't account for irregular expenses, or setting targets that are technically possible but psychologically unsustainable. A budget that asks you to spend £50 per month on food when you currently spend £300 will fail within a week — not because you lack discipline but because the target was disconnected from reality. A budget that accounts for regular monthly bills but misses insurance renewals, car service, holiday costs, and birthday gifts will run over every few months in ways that feel like emergencies rather than predictable expenses. The first task in building a budget that actually works is understanding your true current spending, which requires looking at bank and card statements rather than estimating from memory.

The Categories That Matter Most

Fixed expenses (rent or mortgage, loan repayments, insurance premiums, subscriptions with fixed amounts) are the easiest to budget because they don't change month to month. Variable necessities (food, utilities, fuel, toiletries) require averaging from previous months — look at the last three months of bank statements and divide by three for each category. Irregular but predictable expenses (annual insurance renewals, car maintenance, clothing, Christmas, holidays) are where most budgets break down. The solution is to estimate these annually and divide by 12, setting aside that amount each month even if the expense doesn't occur that month. This turns irregular expenses into a predictable monthly amount and eliminates the feeling that money is disappearing unexpectedly.

Building In Breathing Room

A budget with no slack fails at the first unexpected expense. The classic recommendation is to save 20% of income, but for someone with significant debt or a tight income, this figure needs to scale to what's achievable. The more important principle is that the budget must balance — income must exceed planned spending — and there must be a category for unexpected costs. Even a small buffer of £50–£100 per month for unexpected expenses reduces the likelihood that an unforeseen bill derails the entire budget. Over time, as higher-cost obligations are paid down or income increases, the breathing room expands and saving becomes easier. Starting with a budget that works rather than one that's optimal is more important than precision in the early stages.

Reviewing and Adjusting as You Go

A budget is a living document, not a fixed plan. Monthly review — comparing actual spending against planned amounts in each category — tells you which categories are consistently over or under. Categories that are consistently over either need their budget raised (if the spending is genuinely necessary) or need behavioural change to reduce them. Categories that are consistently under might be over-allocated, freeing up money to direct elsewhere. A quarterly review of the overall budget structure — checking whether your income, fixed expenses, and goals have changed — keeps the budget aligned with reality. The goal isn't to hit every number perfectly every month; it's to maintain enough awareness of the pattern that you can make informed decisions rather than reactive ones.