I once budgeted carefully for a car purchase and felt very sensible about it. Monthly payment: affordable. Insurance: checked. Fuel: approximated. I owned the car for three months before an advisory on the MOT turned into a repair bill I had not budgeted for at all. Then the insurance renewal came back 30% higher than the quote I had used. Then I actually calculated the fuel I was spending commuting and realised I had based my estimate on a shorter drive than I actually did. The monthly payment was the smallest part of the total cost. I had optimised for the one number I could see clearly and ignored everything around it.

Why the Monthly Payment Is the Least Useful Number to Focus On

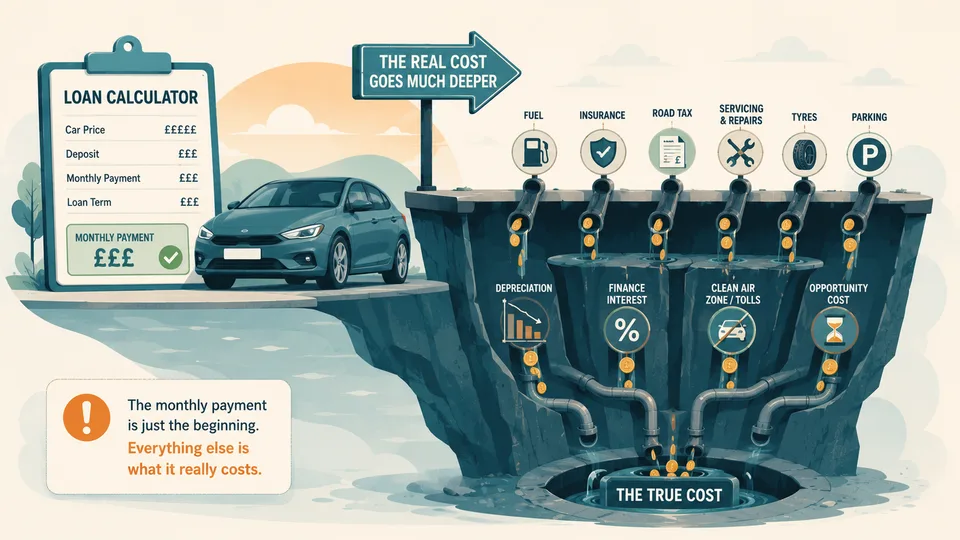

Car finance deals are designed to make the monthly payment look manageable. A £25,000 car on a four-year PCP deal at 8% APR might require £420 per month — a figure many buyers can make work. But that figure captures only the finance cost. Running costs for a typical family car in the UK add between £300 and £700 per month depending on usage, the car's fuel efficiency, insurance group, and maintenance history. The total cost of ownership is closer to £700–£1,100 per month for a mid-range car — a meaningfully different number than the payment alone. Evaluating affordability on the monthly payment is like judging a restaurant bill by the price of the main course.

Depreciation: The Invisible Cost That Dwarfs Everything Else

A new car loses roughly 15–35% of its value in the first year. By year three, most cars have lost 40–60% of their purchase price. On a £25,000 car, that is £10,000–£15,000 in depreciation over three years — approximately £280–£420 per month, every month, simply sitting in the garage. Depreciation is easy to ignore because it does not appear as a direct expense in any bank statement. It is a paper loss until the moment you sell. But it is real money, and on a new car it dwarfs insurance, fuel, and servicing combined. This is why a two or three-year-old car with a full service history often represents significantly better value than new: someone else absorbed the steepest part of the depreciation curve.

The Annual Costs That Never Make It Into the Budget

Beyond the monthly payment and fuel, several costs are paid annually and therefore get mentally filed under "occasional" rather than incorporated into a true monthly cost: road tax (£0–£620 per year depending on emissions for petrol and diesel cars registered after 2017), MOT testing (£54.85 maximum for the test itself, plus any repair costs), servicing (£150–£500 per year for a typical car), and tyre replacement (two to four tyres every three to five years at £60–£200 each). Dividing each of these by twelve and adding them to the monthly total gives a more honest picture. On an older or higher-mileage car, breakdown cover is worth adding too — typically £60–£150 per year.

Fuel Costs at Real-World Economy, Not Claimed Economy

Manufacturers' quoted fuel economy figures are determined under laboratory conditions that do not reflect normal driving. Real-world fuel economy is typically 20–30% worse than the official figure, and worse still in urban driving with frequent stops. A car claimed to do 50 mpg might achieve 36–40 mpg in real use. To estimate your actual fuel cost, take your realistic weekly mileage, divide by your expected real-world mpg, multiply by the price per litre, and convert from gallons to litres. For an electric car, multiply kWh per mile by your home electricity rate — though charging on public networks at peak rates can be substantially more expensive than home charging. Use a fuel cost calculator with your actual commute mileage and the car's real-world mpg to get a number worth budgeting from. Fuel is one of the few running costs you can influence through vehicle choice, so it is worth modelling with realistic rather than optimistic figures.

Insurance: The Cost That Changes Without Warning

Car insurance is required by law and priced individually based on your age, address, driving history, car model, annual mileage, and where the car is kept overnight. Quotes vary enormously between providers for identical risk profiles — comparison sites consistently surface differences of £200–£500 per year. Insurance premiums also change at renewal, sometimes significantly, regardless of any claims. Switching providers at renewal rather than accepting the automatic renewal quote saves the average driver around £100–£200 per year. When budgeting for a new car, always check actual insurance quotes for that specific model before committing — the difference between insurance groups can be £400–£800 per year on similarly priced cars.

Running the Numbers Before You Commit

A realistic car budget has seven components: finance payment or opportunity cost of capital if buying outright, depreciation, insurance, fuel, servicing and MOT, road tax, and a tyre and repair reserve. Adding them together often reveals that a cheaper car with lower depreciation and better fuel economy costs meaningfully less per month to own than a more expensive car with a similar monthly payment. A car affordability calculator that includes all seven cost categories gives you the honest monthly figure before you commit. The payment is engineered to be accessible. The total cost of ownership is what determines whether the car actually fits your budget over the years you own it.

What to do next

Use the ideas above as a starting point — then connect them to your own numbers and related guides on Calc It Anything.

- Read the personal finance and money management guide for the wider cluster.

- Compare with The Cost of Waiting to Save: How Delays Destroy Wealth.

- Compare with Why Lifestyle Inflation Sneaks Up on Almost Everyone.

- Run the relevant calculator on this site with your own inputs before making a decision.

Related reading

- personal finance and money management guide

- The Cost of Waiting to Save: How Delays Destroy Wealth

- Why Lifestyle Inflation Sneaks Up on Almost Everyone

- Why Your Pay Rise Feels Smaller Than Expected

- Complete Budgeting, Saving & Personal Money Management Guide

- Complete Compound Interest, Investing & Wealth Building Guide

For official UK context, see MoneyHelper UK.

Frequently asked questions

Does lifestyle inflation always follow a pay rise?

Not inevitably, but it is the default unless you decide allocations before the new salary lands. Automating savings and fixed goals on payday reduces drift into upgraded spending.

How much does starting to invest late actually cost?

It depends on monthly amount, return assumption, and years left. The gap grows non-linearly because early contributions compound longer — run your age and contribution in a compound interest calculator rather than guessing.

What is a sensible first step after reading this?

Pick one number to model — retirement age, savings rate, or debt payoff — in the relevant calculator, then adjust one habit for the next pay cycle. Small consistent moves beat perfect plans you never start.